The Proposals of the Finance Bill, 2026 which was released on 30th April 2026 are expected to become effective once it is passed into Law/Act of Parliament. Accordingly, the effective date of parts of the Bill is 1st July 2026 while the other parts are scheduled to take effect from 1st January 2027.

The Bill affects tax Laws across Board and in this release, we provide a summarized review for purposes of bringing out the proposed changes therein in very common terms.

I) FINANCE BILL 2026 UPDATES

1. DUE DATES FOR FILING TAX RETURNS

The new proposal here seeks to change the annual income tax filing deadline from six to four months after close of year of income. It also seeks to give the Commissioner powers, through a notice, to require a taxpayer to file annual income tax returns by end of the fourth months after end of year of income. While coinciding with the deadline for payment of balance of tax, this move appears to favor revenue authority collection in terms of the timeframes. For businesses, the proposed change would put pressure on operations for early closure of financial audits.

In addition, the proposed change will require that tax payers who file nil returns to do so within one month after the year end.

Proposed effective date is 1st January 2027. – Sec 52

2. CARD TRANSACTIONS & COST OF SOFTWARE

In a move seen likely to widen the tax net in the digital payment sector, management or professional fees would include interchange fees and merchant services fees in the card transactions for payments. This has clarified the position on the said items under the Law.

In a move that could increase the cost of software in the Country, the definition of royalties is expanded to include acquisition of software for distribution where regular payments are made through the distributor. In addition, payment for use of digital platforms, payment networks, payment card scheme, payment processing systems, or settlement systems have been included in the definition of royalty.

Proposed effective date is 1st July 2026.

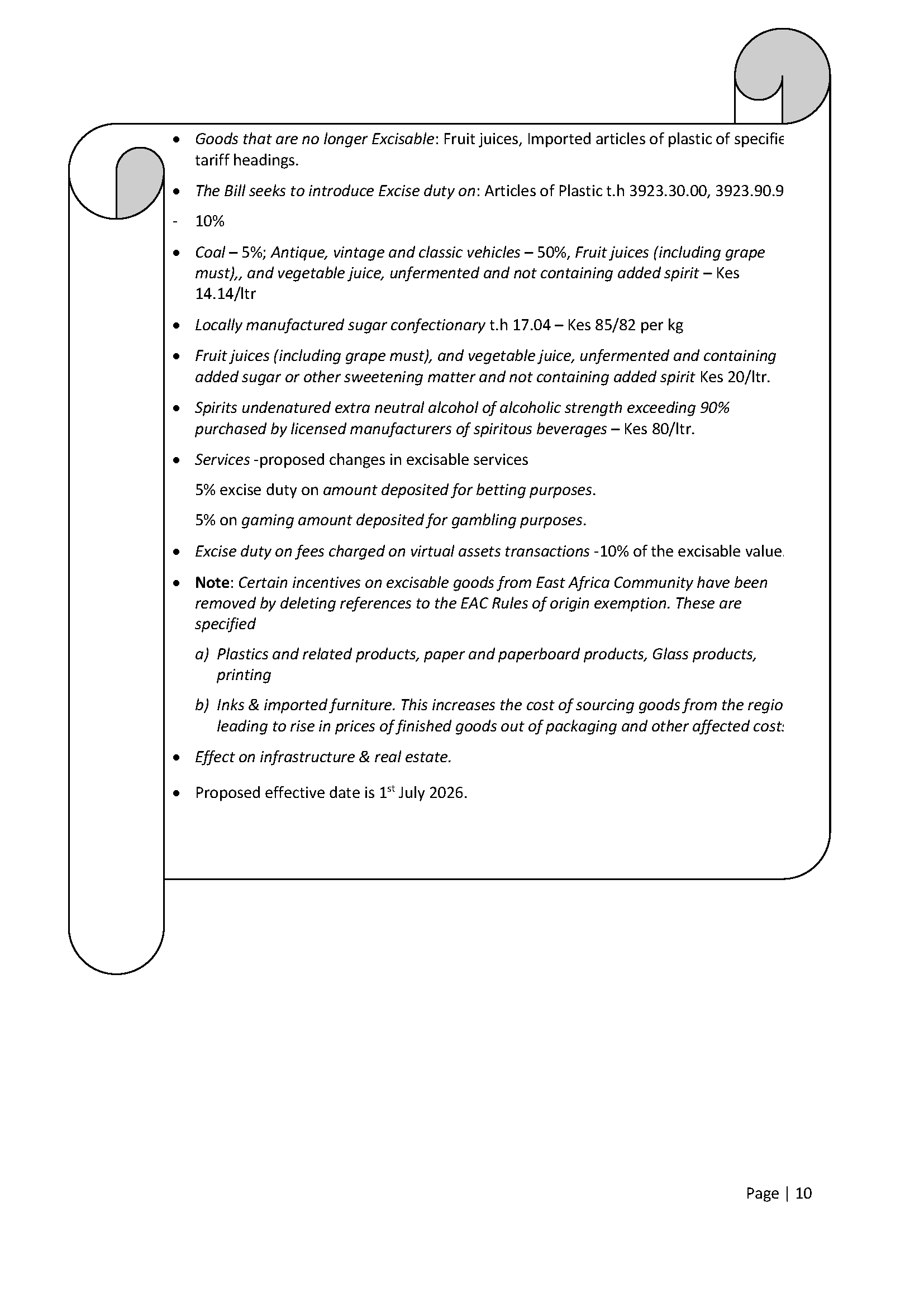

3. BETTING/GAMBLING

The Bill has re-introduced “winnings” which excludes the amount staked or wagered and broadens the definition of the term withdrawals under the Gambling Control Act of 2025.

Withholding tax at the rate of 20% on winnings is sought to be reinstated both for residents and non-residents a move that will affect betting, gaming and lottery sectors.

There are also proposed changes in regards to Excise duty. The amount deposited includes money paid, transferred or credited whether in cash or cash equivalent and not only restricted to money put in a wallet or converted into tokens. This is a move for a more uniform tax base on betting & gaming with a higher cost on players.

Excise duty would also apply to fees charged on virtual asset transactions.

Proposed effective date is 1st July 2026.

4. INSURANCE COMPANIES

Ss 45 of the Insurance Act covers long-term insurance classes including life insurance fund. The Bill propose to replace life insurance fund with statutory fund to include a broader level of business. It proposes to replace references to “life insurance” appearing the income tax Act with the term “statutory fund”.

Proposed effective date is 1st July 2026.

5. SCRAP METALS

Income from sale of scrap metals will now be subject to withholding tax at the rate of 1.5%. This is a re-introduction of the requirement which was repealed under the Finance Act t, 2025.

Proposed effective date is 1st July 2026.

6. MTUMBA CLOTHING

The Bill has proposed to tax the income from imported worn cloth, footwear and other used articles at 1.5% effective rate of taxation which will be final, and taxed at the importation point before goods are released. However, this is seen as tax on unsold stock, whereby a clear conflict could arise between taxation and revenue recognition especially where goods remain in stock for a long period of time.

There is also no clear definition of customs value.

◘ Likely implications:

i) Higher cost of importing second hand clothing thus higher retail prices;

ii) Reduced margin for traders;

iii) A likelihood of increased demand for locally produced goods, which could be a welcome development by local producers.

Proposed effective date is 1st July 2026.

7. DIVIDEND PAYOUT

7.1 The Bill has proposed deleting of withholding tax rate of 5% on dividends paid to Citizens of the East African Community Partner states. The bill, if enacted would see dividends paid to all non-residents treated to a withholding tax of 15%. This further diminishes attraction of EAC citizens to Kenyan investment and dwindling harmony across the Partner States.

7.2 Non-distribution of Dividends by Profitable Corporates

If the Bill passes into Law, the revised concept of dividends which are deemed to have been distributed, for income tax withholding purposes, may be applied by the Commissioner to not more than 60% of the income of the company if a Company fails to distribute its income twelve months following its financial year end. The Commissioner will treat 60% of the Income as dividends on the assumption that the company could have distributed such profits to its members and withheld the applicable tax. Previously, the provision allowed the Commissioner to deem up 100% of the income as dividends.

We could see more assessments of deemed dividend with the change in this proposed change which is targeting corporates retaining earnings without clear need for it. Companies may now have to demonstrate plans on capital expenditure, working capital needs or debt obligations. Thus, Companies may have to refresh or establish dividend policies, capital allocation strategies and prepare better tax plans.

Proposed effective date is 1st July 2026.

8. SHIP & AIRCRAFT

The bill proposes to abolish withholding tax on payment, for gains or profits, made to ship and aircraft owners and rather, they are required to remit full tax within five days of receipt of payment for port services not including transshipments.

Proposed effective date is 1st July 2026.

Additionally, if the bill is enacted, payments by the national carrier for specialized technical, maintenance, compliance and training or digital support services which are not locally available, and rendered by a non-resident will now be treated as management and professional fees which are subject to withholding tax. This repeals provisions in the Finance Act, 2025.

Proposed effective date is 1st July 2026.

9. GRATUITY

In regard to gratuity or similar payments made by an employer in respect of employment or services which is paid into a pension scheme, the bill proposes (new restriction) that such payments would qualify for tax exemption if an employee was engaged under a continuous contract of employment for a minimum of three years. Therefore, under the proposal, payments made on less than three years engagement would not qualify for exemption and thus to be treated as taxable.

It further proposes a new condition for contribution arising from gratuity payments by an employer. Such contributions should be equal to or lower than 31% of the basic salary of the employee; except if the person is eligible for deductions over contributions made to a registered pension or provident fund. Notably, the proposed move to expand the scope of exemption to payments made to other schemes (other than registered schemes) within the new restrictions.

Proposed effective date is 1st July 2026.

10. BENEFITS AS A RESULT OF DEATH

The bill proposes to exempt pension related benefits paid to beneficiaries or dependents of a deceased member a registered pension fund, provident fund, individual retirement fund, public pension scheme or NSSF beyond the current tax exemption on pension related benefits.

Proposed effective date is 1st July 2026.

11. TRUST INCOME

As a matter of clarification, the bill states that once tax is paid by a trustee, executor or administrator, beneficiaries will not be subject to further tax on distributions thus received. When taxed amounts are paid out to a beneficiary, dividends or interest thereof earned by the trustee, executor or administrator shall not be subject to further tax.

12. COMPANY SHARES

In the current set up, Capital Gains tax is imposed on indirect transfers where shares in a foreign entity derive more than 20% of their value from immovable property which is in Kenya.

In the proposal, Capital Gains tax is imposed on indirect or direct transfers of interest in a foreign entity being sold and which derive more than 20% it’s capital from property, other than immovable property, which is based in Kenya.

Further, it proposes that gains from sale of shares by a non-resident person where shares derive their value in Kenya or sale results in a change of group membership of a Company resident in Kenya or ownership of title in or interest In property located in Kenya will be charged to CGT.

This would affect investor strategy in exiting investments in Kenya. Proposed effective date is 1st July 2026.

8th schedule

13. REAL ESTATE INVESTMENT TRUSTS (REITS)

Under a new proposal, gains resulting from transfer of property to a registered REIT would be exempted from CGT. This move will encourage REIT structures due to resultant tax efficiency on the part of property owners and developers putting more assets therein.

Further, it seeks to amend Ss 96A of the Stamp Duty Act and exempt transactions relating to transfer of beneficial interest in a property to a REIT. The investment into a REITs structure thus becomes more attractive due to the tax efficiency encouraging the REITs investment in the Country.

Proposed effective date is 1st July 2026. – Schedule 1

14. TRANSFER PRICING & THIN CAPITALISATION

14.1 Country-by-Country Reporting

For clarification, the filing of country-by-country report would under the new Bill require filling of a master file and a local file as may be specified by the Commissioner by either the ultimate parent entity or constituent entities in Kenya.

In a move to align to OECD BEPS Action 13 framework, the bill proposes to change the definition of an Ultimate Parent Entity (UPE) to state that a UPE is a constituent entity of multinational entity group that; holds sufficient ownership interest whether directly or indirectly in one or more other group entities, it prepares consolidated financial statements under applicable financial standards or would be required if its equity was publicly traded; and is not itself controlled whether directly or indirectly by another constituent entity within the group. This aims at aligning to global standards.

Proposed effective date is 1st July 2026.

14.2 Lending/leasing business

As a matter of clarification, the exemption from thin cap rules applies on non-deposit taking institutions in the business of lending, leasing, or both lending.

15. RENTAL INCOME

15.1 Residents

The Bill proposes to reinstate 10% rate on residential rental income up from 7.5% thereby increasing the tax burden for residential property owners.

15.2 Non-residents

Under the proposed terms, a non-resident person earning rental income from Kenya is required to pay a non- resident rental income tax. The non-resident will be required to register with KRA under a simplified framework, pay the tax due and file returns by the 20th day of the month following receipt of rent. Registration will not be required where rent is received by a resident person on behalf of the non-resident landlord. This move would improve compliance and reduce leakage.

The non-resident rental income tax is a final tax.

Proposed effective date is 1st July 2026.

16. MINING AND PETROLEUM OPERATIONS BY NON-RESIDENTS

The Bill proposes 15% specific tax on repatriated income received by non-resident mining licensees in Kenya. Conversely, the bill proposes to reduce the corporate tax rate for non-resident petroleum contractors from 37.5% to 30%.

For non-resident Petroleum contractors operating through permanent establishment in Kenya, the bill introduces 15% tax on repatriated income under Ss 7B of the Income Tax Act.

Proposed effective date is 1st January 2027.

II) OTHER PROPOSED MEASURES & ADJUSTMENTS

1. INDUSTRIAL BUILDING DEDUCTION (IBD)

The Bill seeks to clarify that Industrial building deduction at 10% is to be claimed per year in equal instalments, a provision currently not clearly provided.

2. INSTALLMENT TAX

Section 12(1)(a) of the Income Tax Act has been replaced with a revised clause indicating that a person is exempted from paying instalment tax if to the best of their judgement, they will not have income chargeable to tax during that year other than emoluments.

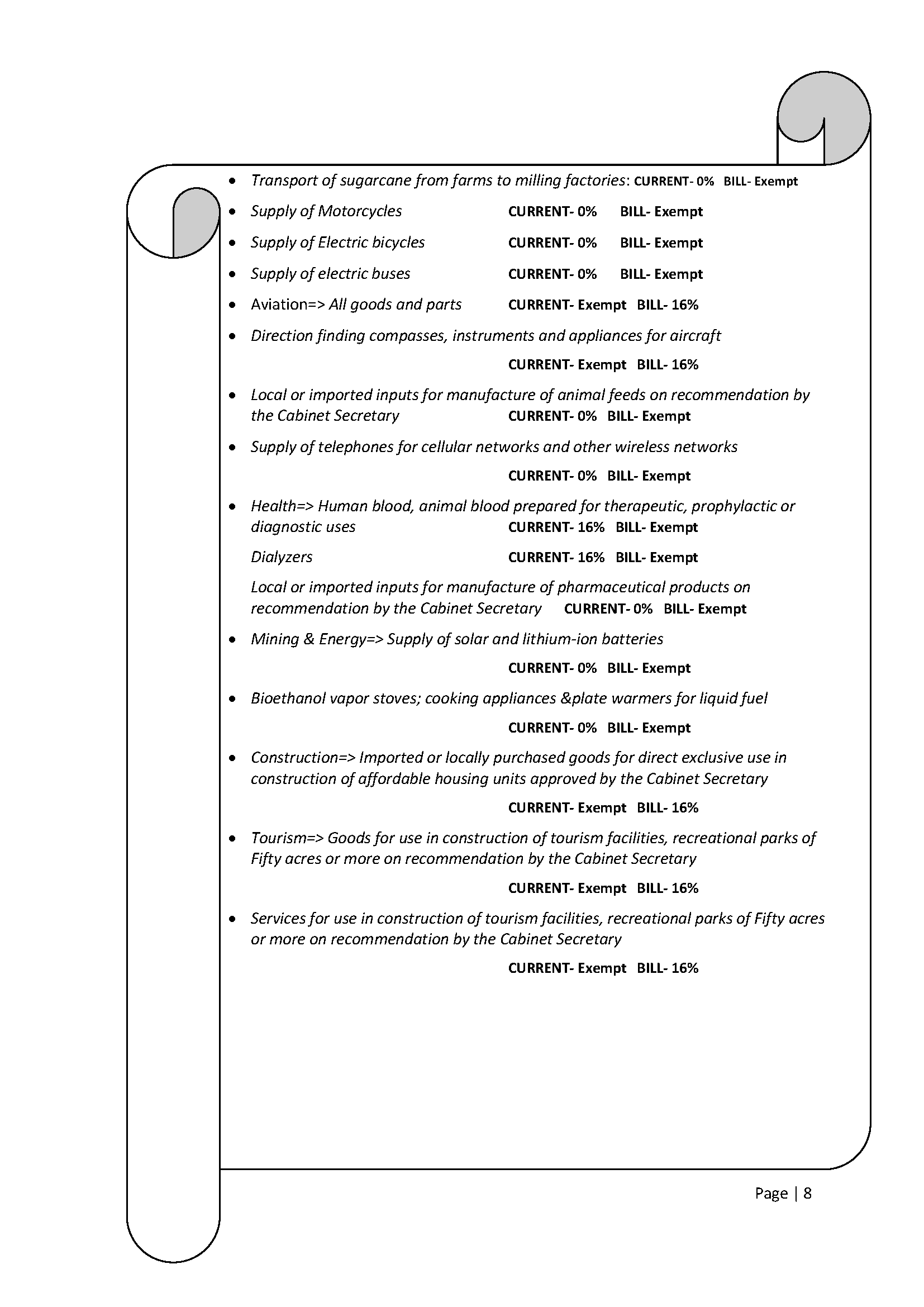

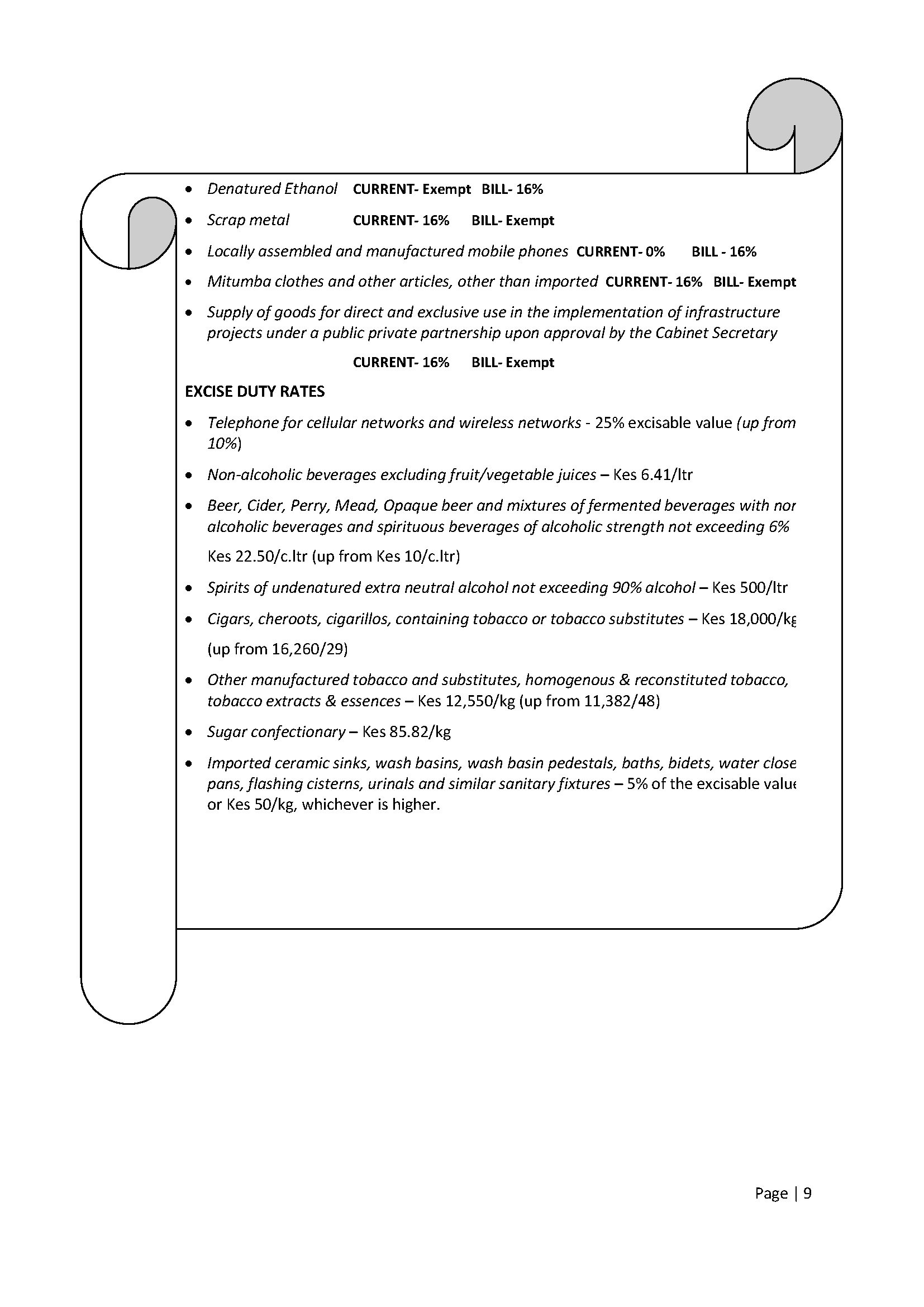

3. VALUE ADDED TAX ACT

Ss 17A is introduced to the VAT Act to address the issue of input tax on taxable supplies that eventually become tax exempt and remain unsold. The person would be required to account for an amount equivalent to the input tax attributable to the unsold supplies in the tax period within which they become exempt. This would safeguard revenue by preventing the retention of input tax credits on supplies that are no longer taxable.

4. TAX REFUNDS- VAT on bad debt

The period within which one can claim a refund of VAT on bad debts is proposed to be reverted from two years back to three years. By prolonging the period before which a taxpayer cannot claim relieve from tax debt arising from bad debts, this proposal would negatively affect cashflow for taxpayers.

5. TAX INVOICING/AUTO-POPULATED RETURNS

As proposed, all persons (registered for VAT or not) will be required to issue tax invoices at the point of making supplies which will align with the Tax Procedures Act.

The Bill proposes to ease the requirements for issuing a tax invoice showing the tax amounts thereof. As proposed, a tax invoice does not have to necessarily show the tax amounts unless the invoice relates to a taxable supply.

6. EXEMPT FINANCIAL SERVICES

In terms of exempt financial services, the Bill seeks to clarify on exclusions from exemption which include digital and platform based financial services; money transfers, payment processing, settlement, merchant acquiring, gateway or aggregation services offered through a software for fee or commission by a payment service provider. These will not be exempt thus bringing in the taxation of digital economy while widening the tax base. In addition, the Bill seeks to tie tax exempt hire purchase financial charges to transactions by service providers registered under Hire Purchase Act.

7. EXEMPT STOCK

The Bill proposes a restriction in form of an adjustment on the input tax, on supplies in stock which convert from taxable to exempt supplies, previously claimed or offset against input tax. The adjustment will involve re-computation of tax liability assuming that the exempt supplies were exempt when the last tax computation and filing was completed, before the date the supplies became exempt. Any additional tax resulting from this adjustment will be payable.

While this measure is meant to safeguard tax revenues, on the other hand, it will complicate VAT compliance for the taxpayers.

8. EXEMPTION OF TOUR SERVICES

The Bill attempts to define a tour operator as a formally licensed by tourism regulatory authority as the entities exempted under the VAT Act. It also seeks to define in-house supplies as

services provided through operator’s own resources or significantly transformed after being acquired from third parties. Inhouse supplies of such Companies are not tax exempt.

9. GOODS ACCOMPANING RETURNING PASSENGERS

Returning passengers with accompanying imported goods could be happier if the Bill passes into Law as the VAT free threshold would rise from the current $300 to $2,000 provided the passenger was outside Kenya for more than twenty-four hours and goods are declared to a customs officer.

I) MORE UP-DATES

1. NON-COMPLIANCE PENALTIES- ETIMS

As proposed, a taxpayer who fails to issue a e-Tims compliant invoice would be required to pay the higher of:

a) Two times the value of tax due;

b) A fine of Kes 10,000/- for individuals;

c) A penalty of Kes 100,000/- for Companies. This is a move to further enhance e-Tims Compliance and ensuring all transactions will have electronic trace.

It proposes to formalize filing of tax returns based on information provided in the auto-populated returns.

The Introduction of Ss 89(5b) empowers the Commissioner the power to waive wholly or in part penalties and interests not exceeding Kes 2 million either due to an error in the electronic system or as otherwise provided.

2. COMPUTATION OF TIME

Under a new proposal, taxpayers will have 30 calendar days (weekends and holiday reckoned) to object to, or appeal a decision to Tribunal, or the Courts.

3. NON-RESIDENT PIN APPLICATION

The Bill proposes to exempt non-resident persons from obtaining PIN Number when opening a Bank Account.

4. TAX AVOIDANCE

The Commissioners powers to stem tax-avoidance is further reinforced through Ss 18A of the Tax Procedures Act, as proposed. Where the Commissioner is satisfied that a taxpayer benefited from a tax avoidance scheme, a tax assessment will be conducted on the basis of various stated sources. A tax assessment would be issued within five years from the last day of the tax period which the tax liability relates.

The Commissioner could rely on information from employers, banks, e-invoicing platforms to estimate income and tax payable. The burden of disputing a data based assessment falls on the taxpayer upon assessment.

However, the bill proposes to repeal tax avoidance provisions under Section 23 of the Income Tax Act and Section 66 of the VAT Act.

5.

The National Intelligence Service (NIS) is proposed for inclusion in the exemption of excise duty on goods supplied for official use Kenya’s Security and Defense services.

Proposed effective date is 1st July 2026.

6.

Definition of antique, vintage or classic vehicles and criteria based on age and value is sought to be clarified.

7. TAX RATES

IV) EAST AFRICAN COMMUNITY TRADE

IV) EAST AFRICAN COMMUNITY TRADE

Excisable goods from EAC Partner states proposed as not subject to excise duty in Kenya. Local manufacturers may hence face competitive disadvantage as similar goods produced in Kenya are subject to excise duty.

Proposed effective date is 1st July 2026.

V) MOBILE PHONES

Under the proposed amendments, the timing and payment of excise duty on mobile phones changes and it will be payable upon activation of the phone and not at importation or removal from the factory. This would ensure that duty applies on devices actually activated within Kenya although it could raise issues on ascertaining actual phone activation, tax accounting and timing of the remittance. The Cabinet Secretary may however issue regulations to manage this towards enforcing compliance.

Proposed effective date is 1st January 2027.

VI) INFORMATION RETURNS

The Bill proposes that Virtual Asset Providers will file information returns with the Commissioner showing virtual asset users for each calendar year or of those having controlling persons that are reportable users. It also proposes fines for failure to comply.

VII) TAX DISPUTES

The Bill proposes to restrain the Commissioner from issuing an agency notice where the taxpayer has challenged the Commissioner’s decision before a Court or a tribunal.

VIII) IMPORTATION

◘ Steel Products: Proposed deletion of Ss 6A (4) of Tax Procedures Act under international agreement for certain steel products (wire rods) restores applicable import duty rates. This would increase the cost of manufacture reliant on these materials.

◘ The Bill proposes to remove an earlier requirement to produce a Certificate of Origin for any import. The requirement is also provided under EACCMA.

◘ The Bill also propose to reduce the portion of import declaration fees managed in accordance with Public Finance Management framework from 20% to 10%. The funds will only be directed to Kenya’s international commitments.

◘ The Bill further propose to limit offset of tax credit against taxpayer obligation for VAT on importation. Offsets allowed are only against outstanding tax debts and future tax liabilities/instalment taxes.

◘ The Import Declaration fee and Railway Development Levy exemption on aircraft related imports has sought to be narrowed. This may lead to change in prices for air transport and cargo charges and also make acquisition of aircraft more expensive.

Proposed effective date is 1st July 2026.

IX) IDF/RDF ON MOBILE PHONES

Under the new proposals, importation of telephones designed for cellular/wireless networks will be exempt from import declaration fee and Railway Development levy. This may lower retail prices of phones and improve access to the facility.

Proposed effective date is 1st January 2027.

X) TAX AMNESTY

The Bill proposes to reintroduce tax amnesty on all tax obligations for periods up to 31st December 2025. The waiver, if enacted will be automatic, meaning no need for formal application. However, only taxpayers who have settled all principal taxes accrued on or before the indicated date would qualify for a waiver of penalties and interests.

Waiver of penalties and interest where a taxpayer has outstanding principal tax may be sought through an application to the Commissioner and entering a structured payment plan whereby such plan supports full settlement as at 31st December 2026.

This will provide an opportunity to taxpayers to comply and eliminate exposure at a reduced cost.

XI) LEVIES & FEES

Under the Bill, the scope of imposition of levies and fees to cover anti-adulteration levy, processing fees on duty free motor vehicles and export and investment promotion levy will be expanded.

Disclaimer: This update is meant to highlight updates in regards to the Kenya Finance Bill, 2026. It should not be considered as a substitute for professional advice. The Firm, its Partners, Associates, employees and/or agents shall not accept any liability for the consequences of anyone acting, or refraining from acting in reliance on the information herein or any decision arising therefrom. We advise that you seek professional advice on areas that may be of importance to you.

Prime Welsch Consulting LLP is based in Nairobi, Westlands, Madonna House, 3rd Floor Suite 317 and offers professional services to businesses and organisations including Tax Compliance & Advisory, Transfer Pricing, Cross Border Transaction structuring/re-structuring, Accounting, Company Secretarial, Governance, Human Resource support. A full description of our services is featured on our website www.primewelsch.com.

Any enquiries are welcome through our email address;

EMAIL US